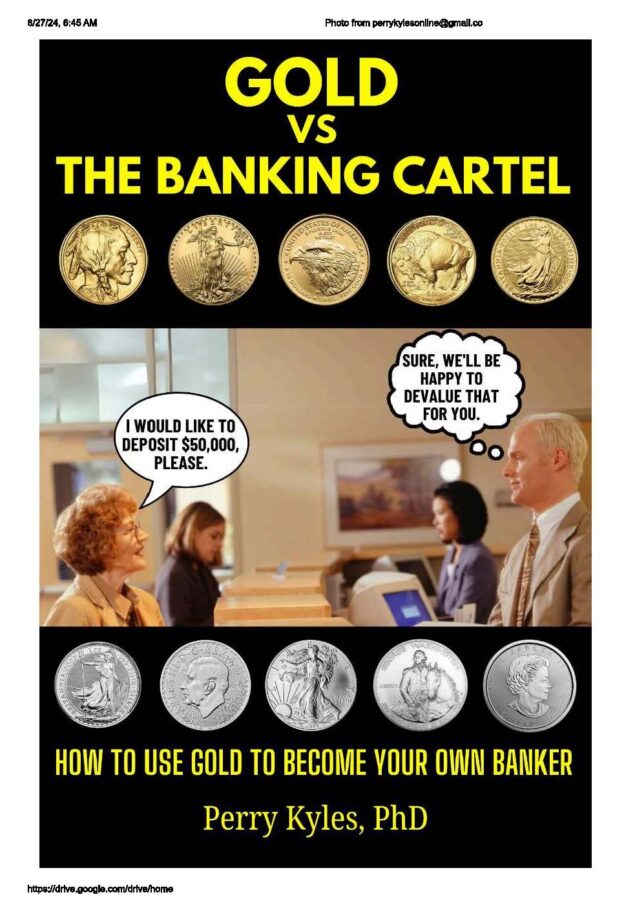

Gold vs. The Banking Cartel delivers a compelling message to all Americans—an urgent call to safeguard the purchasing power of your hard-earned dollars. In the ever-evolving financial landscape, one thing remains constant: the need to protect your wealth. But how can this be achieved? This book argues persuasively that the answer lies in a strategy as old as civilization itself: investing in gold and silver.

The Roots of Financial Instability

The journey begins with a critical examination of a pivotal moment in American history—1971, the year the United States abandoned the gold standard. This decision, as the book highlights, opened the floodgates to reckless government spending and debt accumulation.

Today, we face the consequences of these actions, as our national debt continues to soar.

The book draws a powerful comparison between modern America and the decline of Ancient Rome or Zimbabwe’s economic collapse, underscoring the urgency of preparing for potential financial turbulence.

Exposing the Banking Cartel

Gold vs. The Banking Cartel exposes the power of the banking cartel.

The book reveals how this cartel, in collusion with Wall Street and the Federal Reserve, has manipulated the financial system, leading to the devaluation of the dollar and erosion of Americans’ savings.

Through a detailed exploration, the book provides a clear understanding of the impact of hyperinflation on everyday life and the importance of hedging against it with precious metals.

Gold vs. The Banking Cartel warns of economic instability and the need for alternative investments like gold. Instead, the book argues for the necessity of diversifying into gold, a tried-and-true store of value.

The Path to Financial Freedom

Gold vs. The Banking Cartel provides a practical guide to gold investing, covering bullion, collectibles, and IRAs. By preparing yourself with the knowledge provided, you can avoid common pitfalls and take control of your financial future.

Finally, the book makes a strong case for why gold should be the cornerstone of your liquid assets. It offers practical advice on how to buy gold wisely, avoid scams, and even become your own banker.

For those ready to take control of their financial destiny, Gold vs. The Banking Cartel is a must-read. This brief yet powerful book equips you with the knowledge and tools to protect your wealth in an uncertain world.

Invest in your financial future with Gold vs. The Banking Cartel. Choose between the physical copy ($18.95) or audiobook ($8.95).

As you embark on this journey, consider taking the next step by investing in gold and silver through a trusted source.

To begin, visit The Gold Marketplace, LLC to explore a wide range of precious metal products.

Moreover, our expert team is here to ensure you make the best choices for your future. So don’t wait—protect your wealth today with The Gold Marketplace, LLC.

RECEIVE THE EBOOK FREE! CLICK HERE!